Below are verified examples of users who successfully recovered funds, reversed limitations, or forced PayPal to back down. Methods range from UK Financial Ombudsman escalations and government bodies to small claims pressure and direct social media exposure. Each case is shown with the original screenshot evidence.

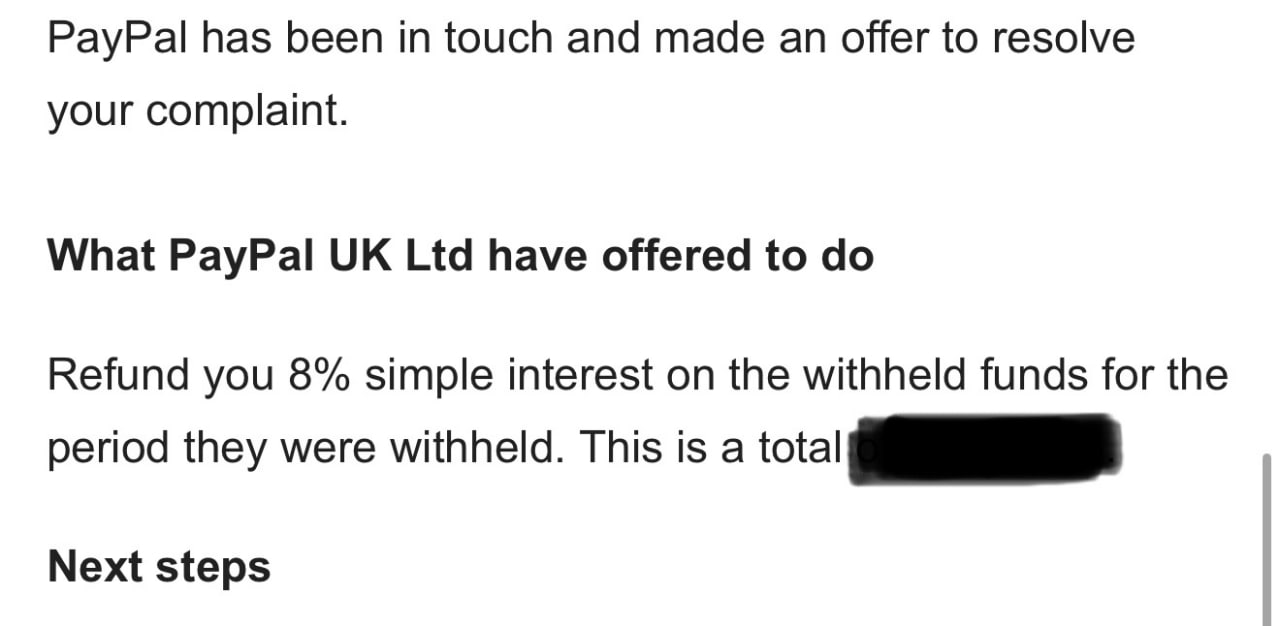

Financial Ombudsman forces PayPal to pay 8% statutory interest

A UK-based user escalated their complaint to the Financial Ombudsman Service (FOS) after PayPal refused to release withheld funds. The FOS contacted PayPal and obtained a formal offer: a full refund of the withheld amount plus 8% simple interest calculated from the date the funds were first held. The offer letter shown below was issued directly via the FOS portal.

Key takeaway: The FOS can compel PayPal to make pro-active settlement offers that go beyond what PayPal was willing to give voluntarily. Statutory interest at 8% can be a meaningful addition on top of large balances held over extended periods.

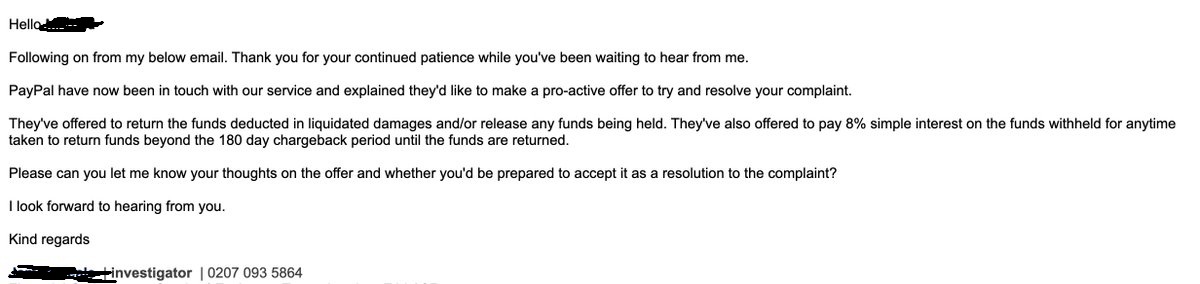

FOS investigator secures full fund return + 8% interest for Mr Reid

In this case, a FOS investigator reached out to the affected user to relay PayPal's settlement offer. The offer included: (1) return of all funds deducted as liquidated damages and/or held funds, and (2) 8% simple interest on the withheld balance for any period beyond the 180-day chargeback window until the money was returned.

Key takeaway: Filing with the FOS puts a named investigator on your case who liaises directly with PayPal. PayPal made this proactive offer only after FOS involvement, not before.

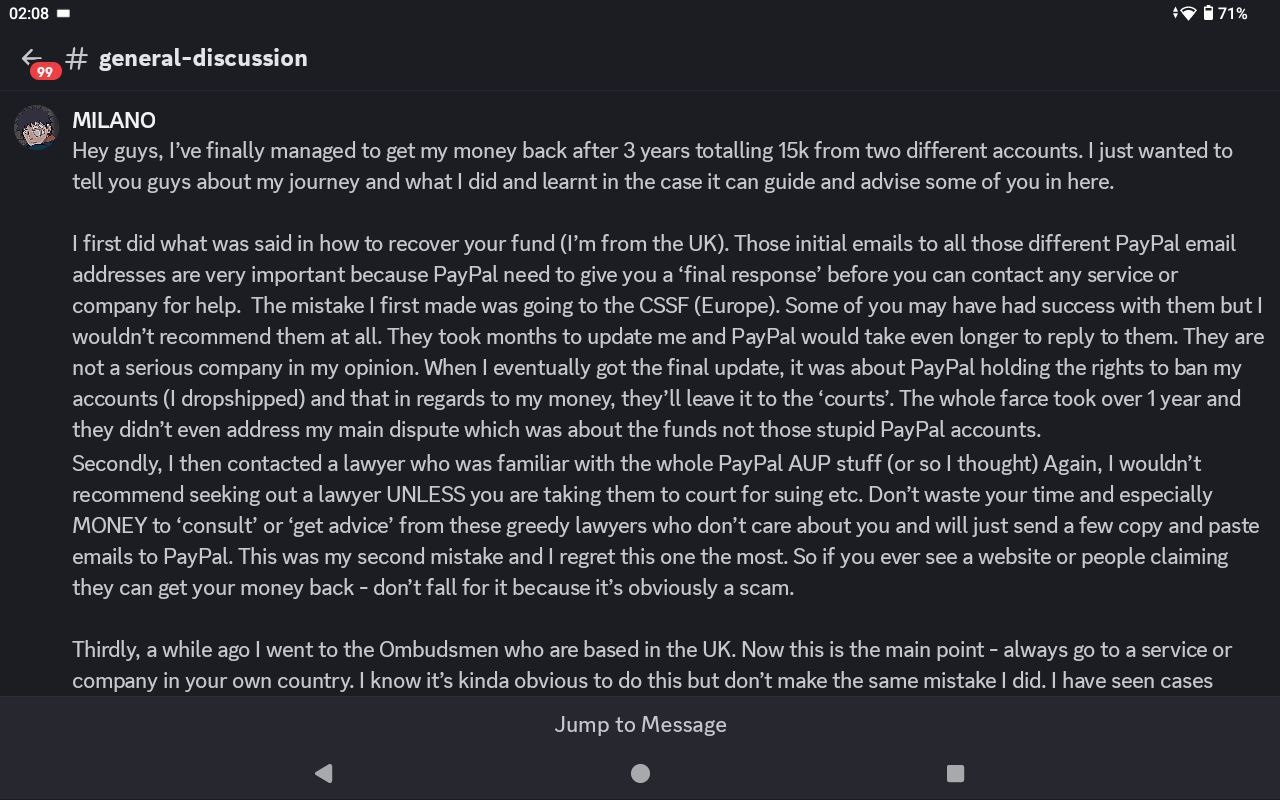

MILANO: £15k from two accounts recovered via UK Ombudsman

Community member MILANO shared their full journey after finally recovering £15,000 across two separate PayPal accounts, three years after the funds were first withheld. Their account is one of the most detailed first-hand walkthroughs we have seen.

Key lessons from their post:

- Don't start with CSSF (Europe): CSSF is slow, unresponsive, and in MILANO's case spent over a year without addressing the core dispute. Not recommended.

- Legal counsel: Be cautious with lawyers unfamiliar with PayPal AUP enforcement. Users report generic, copy-paste outreach that wastes time. Consider counsel mainly for litigation or jurisdiction-specific court work.

- Always go to the Ombudsman in your own country. For UK users this means the FOS. MILANO tried CSSF (Europe) first, a mistake they explicitly warn others against.

- The initial emails to multiple PayPal addresses matter: PayPal must issue a "final response" before the FOS can accept your complaint. Those early emails start the clock.

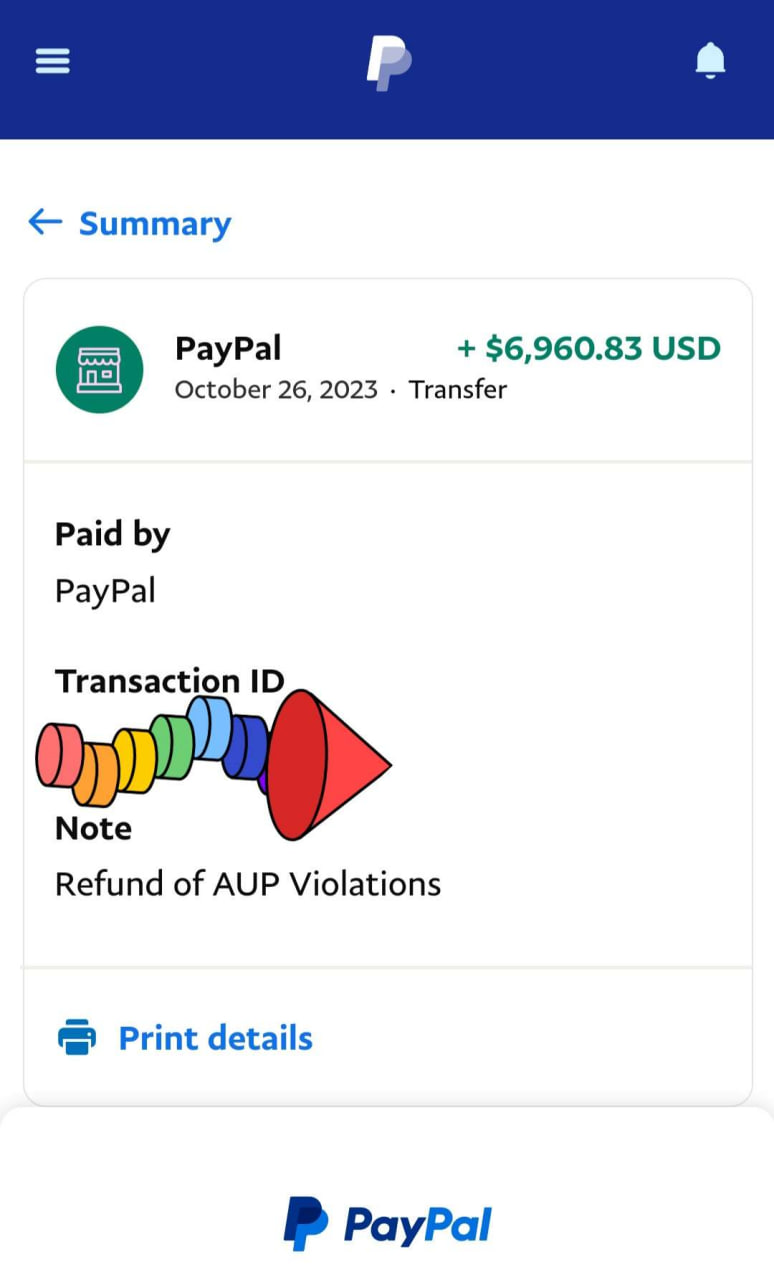

Japanese user recovers $6,960.83 labelled "Refund of AUP Violations"

This PayPal transfer screenshot shows a $6,960.83 USD payment made directly by PayPal, with the note "Refund of AUP Violations". The user is based in Japan and successfully recovered the funds by contacting PayPal through multiple escalation channels and involving a Japanese governmental financial body.

The note itself ("Refund of AUP Violations") is significant: PayPal's own transaction label acknowledges the funds were originally seized under an AUP enforcement action and are now being returned. This is one of the clearest documented examples of PayPal reversing an AUP-based seizure.

Full case write-up: This user documented their entire 2.5-year recovery process, including all steps taken and the governmental escalation pathway. Read the full case record (PDF) →

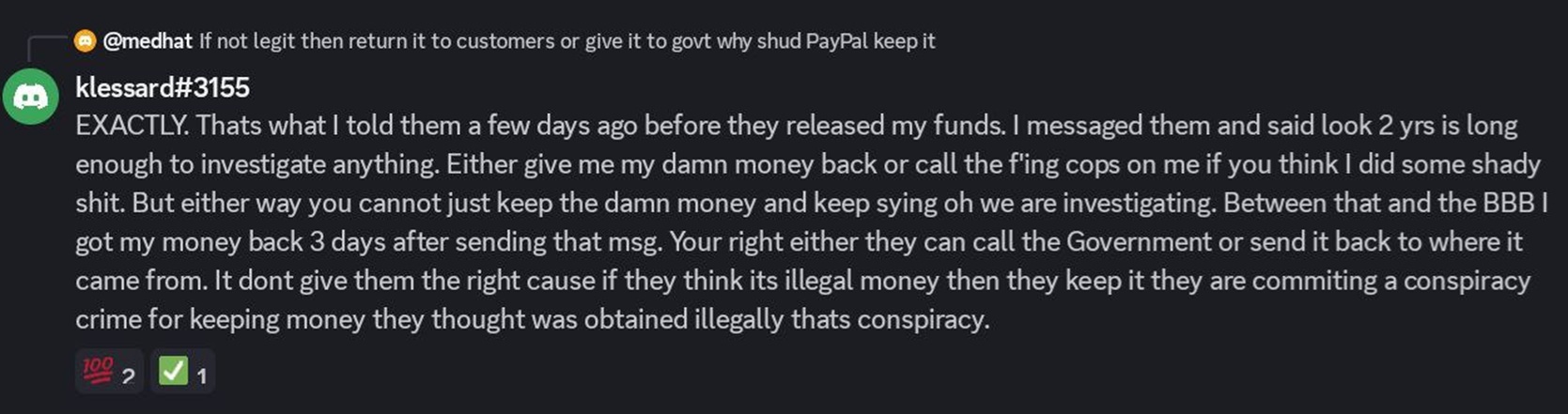

klessard: funds returned 3 days after BBB complaint and firm warning

Community member klessard#3155 had their funds withheld for over 2 years. After exhausting patience, they sent PayPal a direct message: either return the money or involve law enforcement, because they could not keep the funds indefinitely under the guise of an ongoing investigation. They also filed a complaint with the Better Business Bureau (BBB).

The result: funds were released within 3 days of sending that message.

klessard also made a sharp legal point: if PayPal genuinely believed the funds were obtained illegally and chose to keep them rather than report them to authorities, that conduct itself could constitute a form of conspiracy. This framing (holding allegedly illegal money without reporting it) can be a powerful argument when escalating formally.

Key takeaway: A BBB complaint combined with a firm, clear deadline message can produce fast results, especially after long delays. The BBB route is particularly effective in the US because PayPal monitors and responds to BBB complaints to protect their rating.

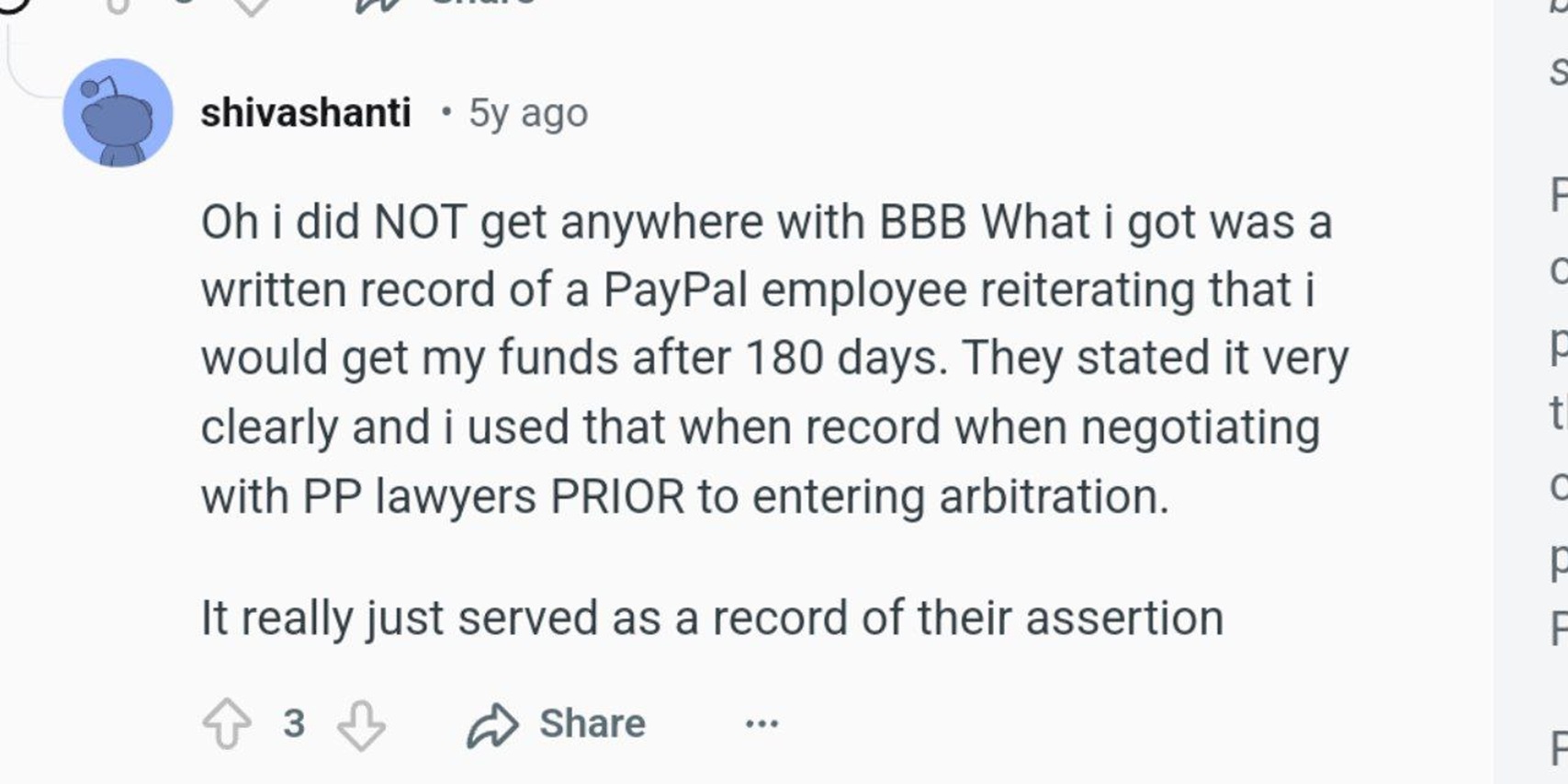

shivashanti: BBB complaint produced a written record that won the negotiation

Reddit user shivashanti did not get a direct resolution from the BBB, but the process produced something arguably more valuable: a written statement from a PayPal employee explicitly confirming that the funds would be released after 180 days. When shivashanti later entered pre-arbitration negotiations with PayPal's legal team, that document was used as evidence of PayPal's own commitment. PayPal's lawyers, faced with their own written assertion, agreed to return the funds before arbitration even began.

Key takeaway: A BBB complaint may not always produce a direct refund, but it forces PayPal to respond in writing. That written response can become a key piece of evidence if you escalate further. Always preserve every written communication from PayPal.

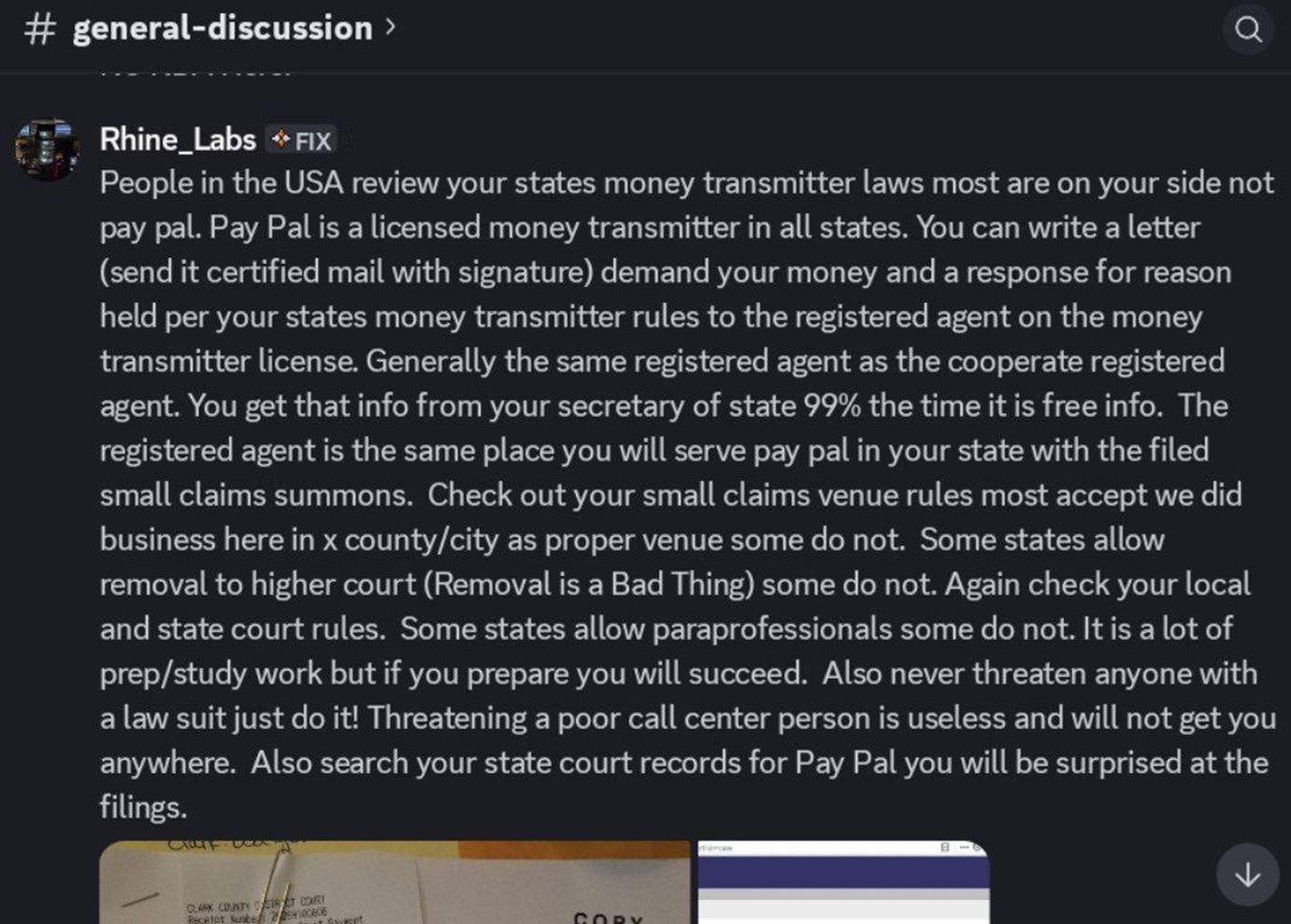

Rhine_Labs: use your state's money transmitter laws and go straight to small claims

Discord member Rhine_Labs shared a detailed breakdown of how US-based users can leverage state money transmitter regulations against PayPal. The core argument: PayPal holds a money transmitter licence in every US state, and most of those states have rules that work in the customer's favour. Rather than waiting for PayPal to respond, Rhine_Labs recommends sending a formal certified letter to PayPal's registered agent (obtainable free from your Secretary of State) demanding your funds and a written explanation under your state's money transmitter rules. The same registered agent is where you serve PayPal if you file a small claims summons.

Rhine_Labs also includes a point consistent with the Moneymaker warning above: never threaten a lawsuit. Just file it. Threatening a call centre agent accomplishes nothing and may be used against you.

Key takeaway: For US users, your state's money transmitter laws are an underused tool. Look up your state's rules, identify PayPal's registered agent via the Secretary of State website, and send a formal certified letter before or alongside any other escalation.

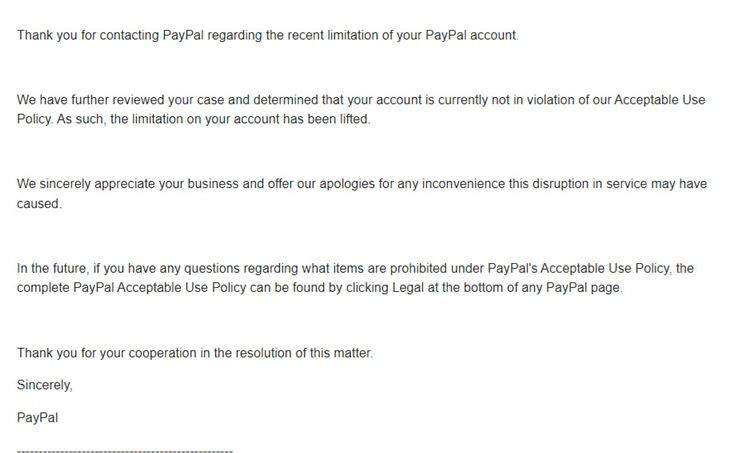

Account reinstated: PayPal acknowledges no AUP violation was found

This user received an unsolicited email from PayPal stating that after further review, their account was found to be not in violation of PayPal's Acceptable Use Policy. The limitation was lifted, and access to the account and funds was fully restored. PayPal also offered an apology for the disruption.

This case is significant for two reasons. First, it shows that PayPal's initial enforcement decisions can be wrong and are sometimes reversed on review. Second, the email itself is a written acknowledgment by PayPal that the original limitation lacked a valid basis. If you are still waiting for a resolution, this type of outcome demonstrates that persistence and formal escalation can prompt PayPal to revisit its own decision.

Key takeaway: PayPal's AUP enforcement is not always final. A formal complaint to a regulator or Ombudsman can trigger an internal review that leads to a full reversal. Keep escalating through proper channels.

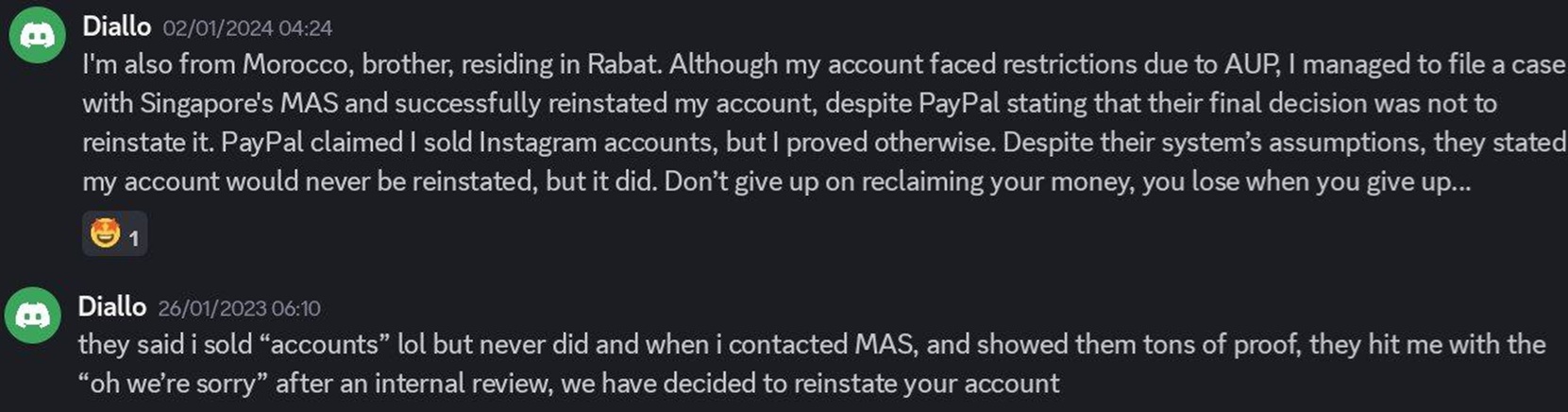

Diallo: MAS complaint helped overturn PayPal's "final" non-reinstatement decision

In this Discord exchange, a user from Morocco, residing in Rabat, explains that PayPal restricted the account under an AUP-related theory and allegedly claimed he had sold Instagram accounts. He says he gathered proof showing that allegation was wrong and escalated the matter to Singapore's MAS.

The striking part is that PayPal had reportedly already told him the decision was final and that the account would never be reinstated. Yet after the MAS escalation and internal review, PayPal reversed course and restored the account.

Key takeaway: "Final decision" language is not always final. When a user puts together evidence and pushes the case to the right regulator, PayPal can be forced to revisit factual assumptions and overturn its own prior conclusion.

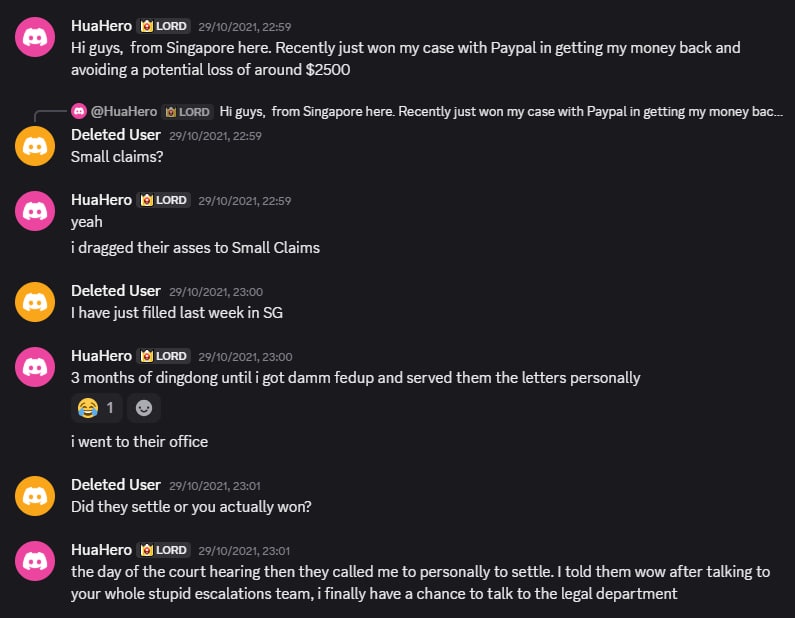

HuaHero: Singapore small claims forced a same-day settlement before any ruling

Here, a user from Singapore says he recovered his money and avoided a potential loss of around $2,500 after taking the matter to small claims. He describes months of back-and-forth, then personally serving letters at PayPal's office before the case reached the hearing stage.

The most important detail is what happened next: according to the post, PayPal called to settle on the day of the court hearing, before the court could issue any ruling. That is strategically important. It fits the pattern users keep reporting: once there is a real risk that a judge might speak on the merits, PayPal appears to prefer settling quietly rather than letting a court say these AUP deductions function as unenforceable penalties.

Key takeaway: Small claims pressure can be enough to recover the money even without a judgment. But this story also helps explain why binding precedent is so hard to obtain: cases may be resolved right before the court has a chance to rule.

Belle Delphine: $90,000 returned after public social media pressure

In 2019, internet personality Belle Delphine had her PayPal account closed without warning and $90,377.58 USD taken, earned from selling her merchandise. In 2024 she tweeted about it and PayPal released her money only after Business Insider and other outlets contacted PayPal for comment.

Delphine herself acknowledged the uncomfortable truth this case reveals: "normal people" without a large social media following would have little chance against the company. The Business Insider article contains two statements from PayPal worth examining closely.

First, a PayPal spokesperson told Business Insider that the company dropped its $2,500 fine policy "about a year ago." This is misleading. The practice of seizing user balances did not stop: what changed was the label. The transaction memo shifted from "AUP damages" to "Loss Recovery." The mechanism, a unilateral balance sweep with no itemised calculation and no proof of actual loss, remains identical. Users continued to report the same deductions after PayPal's stated policy change, as documented across this site.

Second, PayPal told Business Insider that Delphine had violated its rules by selling adult-related physical goods outside the United States. Even accepting that as true, it does not give PayPal the right to retain her funds. A user breaking a platform's rules entitles PayPal to close the account and stop processing transactions. It does not entitle PayPal to appropriate the user's existing balance as its own, without proof of damages, without a calculation, and without any judicial or regulatory order. The violation of a policy is not a licence to seize money.

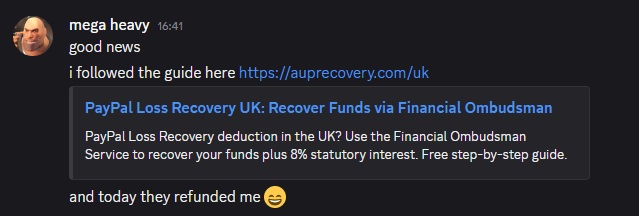

mega heavy: refunded after following the UK guide

A Discord user shared good news after following the UK guide on this site: PayPal refunded their funds. Short, simple, and exactly what the guide is for.

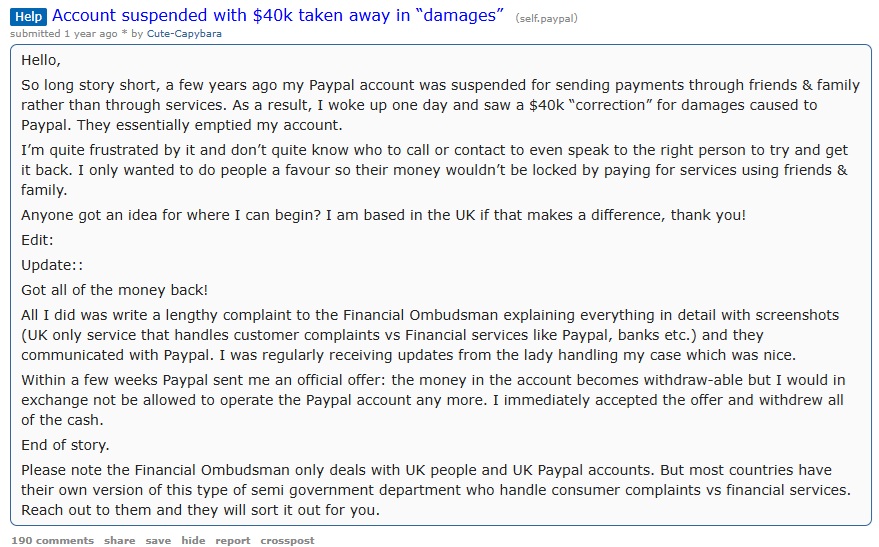

Cute-Capybara: $40k "damages" reversed after UK Financial Ombudsman complaint

The full thread is available on Reddit.

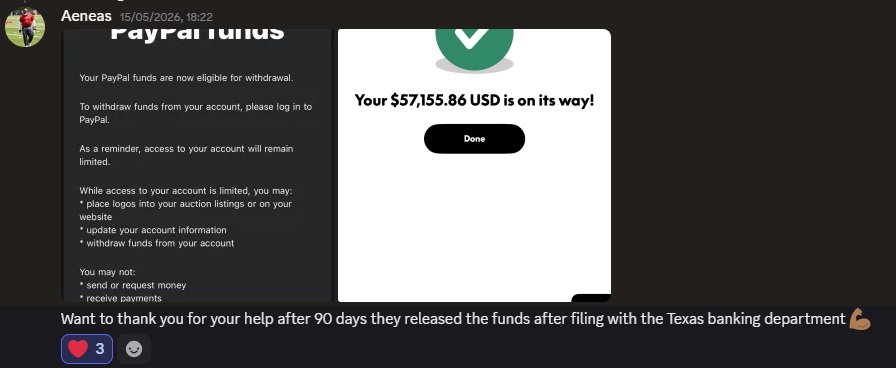

AUPrecovery helps user recover $57k through Texas Banking Department

What these cases have in common

- Escalation works. In every documented case, PayPal did not voluntarily return funds until a formal escalation (Ombudsman, government body, or reputational risk) created external pressure.

- Use your local regulator. UK → FOS. Japan → relevant government body. Going cross-border (e.g. CSSF for a UK user) adds months of delay with no benefit.

- Document everything. The users who succeeded all kept records: emails, PayPal communications, transaction history, and timelines.

- Interest matters. UK FOS cases can include 8% statutory interest on withheld funds, a significant addition for large balances held over months or years.

- When a ruling gets close, settlement pressure rises. Multiple community reports suggest PayPal may reverse course or settle once formal proceedings create a genuine risk of an adverse judicial ruling.