April 2026 update: In written correspondence with PayPal dated April 2026, it was alleged that 3,369 transactions violated the AUP, now citing Nintendo copyright infringement. This is the third time PayPal has changed its stated reason: previously it cited Minecraft's Commercial Usage Guidelines, then copyright infringement in general terms, and now Nintendo specifically. In each instance, no proof of damages was provided, no complaint from the rights holder was produced, and no authorization from the developer was shown. PayPal is not the legal representative of Nintendo or Mojang, has no standing to enforce their guidelines or usage policies on their behalf, and has no standing to adjudicate their intellectual property rights.

In separate communications, PayPal has cited "potential risk" associated with the account. Potential risk is risk that has not materialised. A deduction for a loss that never occurred is a penalty.

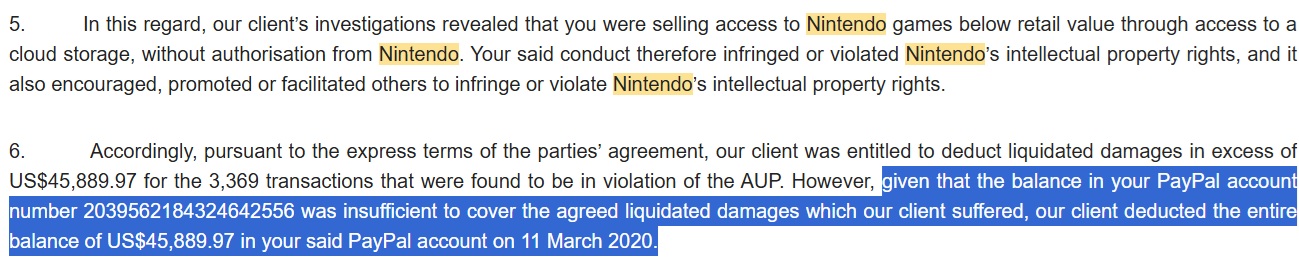

Applied literally, PayPal's own clause of USD 2,500 per violation would produce USD 8,422,500 on 3,369 transactions. No calculation or methodology was disclosed. That figure alone demonstrates the clause bears no relationship to any genuine estimate of loss. In the same April 2026 correspondence, PayPal's external counsel inadvertently confirmed what had always been suspected: that the deduction was not the result of applying any formula. Their own words state that the account balance "was insufficient to cover the agreed liquidated damages" and that PayPal therefore "deducted the entire balance of US$45,889.97." There was no calculation. PayPal took whatever was there. This is the definition of a balance sweep, not a liquidated damages deduction. A genuine pre-estimate of loss is calculated before the fact, not determined by whatever happens to be available.

PayPal has been offered three avenues of resolution: a private settlement under confidentiality (including mutual NDA and non-disparagement), disclosure of the damages it claims to have suffered, or referral to FIDReC so that an impartial third party can resolve this dispute. All three have been refused. In a case plagued by bad faith from the outset, this is yet another act of bad faith.

The funds were taken in the name of damages. No evidence of those damages has ever been shown, yet they refuse to release my funds and allow me to move on with my life. PayPal won't listen to my claims. They have closed every accessible channel of resolution and left me without an affordable venue to enforce my rights. I raised this repeatedly: litigation in Singapore is prohibitively expensive for an individual. They chose not to listen.

This document states allegations and analysis based on currently available information and documents. It is not a court filing, not legal advice, and not a finding of fact.

PayPal Took USD 45,889.97 as “AUP Damages”. No Proof of Any Damage Has Ever Been Shown.

Real example of PayPal Loss Recovery/AUP damages deduction: the older memo "PayPal's damages caused by Acceptable Use Policy violation" and why the deduction is disputed

Ref: LOD108/LT/2026 | Jurisdiction: Singapore

Summary

This matter concerns a debit of USD 45,889.97 labeled as "AUP damages." PayPal has never provided proof of what damages it actually suffered. It has not identified a single transaction causing a specific loss, produced any contemporaneous record of quantified harm, or explained how USD 45,889.97 was calculated. The funds were taken in the name of damages; no evidence of those damages has ever been shown. PayPal has additionally declined to explain transaction-level particulars, the calculation methodology, or the documentary categories relied upon to justify the amount deducted. The claimant operated a digital goods business (TF2 items, Minecraft assets, and Discord roles via DonateBot (donatebot.io, now defunct)). Based on records available to the claimant in PayPal account activity, no chargebacks are shown. PayPal communications later cited Minecraft's Commercial Usage Guidelines and, separately, third-party integration context (DonateBot). PayPal has not provided transaction-level particulars to support either rationale.

I. Requested Outcomes

- Restitution: Return of USD 45,889.97, which PayPal itself acknowledged in writing in September 2025 belongs to me;

- Interest: 5.33% per annum from 11 March 2020 until date of payment;

Additionally:

- Proof of Damages: Documentary evidence of the actual, quantifiable loss or damage suffered by PayPal as a direct result of the alleged AUP violations, including contemporaneous records linking each alleged breach to a specific, identified monetary loss. PayPal cannot retain USD 45,889.97 as "damages" and simultaneously refuse to show what those damages were;

- Transparency: Full disclosure of the specific data inputs, calculation methodology, and internal decision record behind the AUP finding and the debit;

- Record Correction: Removal of adverse internal labels and confirmation regarding whether any adverse information was transmitted to third parties;

- Costs: As appropriate in the circumstances.

II. Documentary Evidence

PayPal Debit Transaction Screenshot

Date: 11 March 2020

Amount: USD 45,889.97

Description: "Daños causados a PayPal por infracciones de la Política de uso aceptable" (Damages caused by an Acceptable Use Policy violation)

PayPal Executive Escalations Email

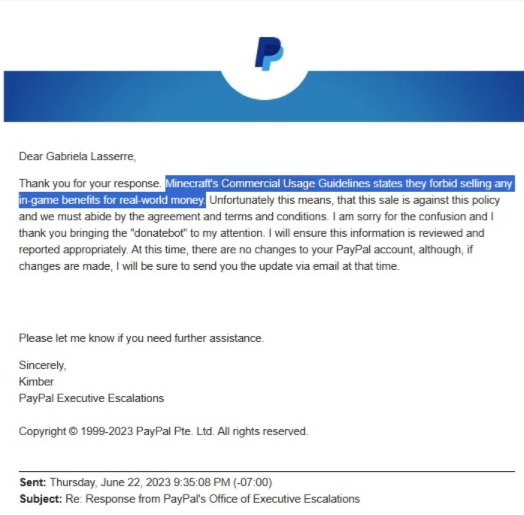

Date: June 2023

Key Statement: PayPal cited Minecraft's 'Commercial Usage Guidelines' and the prohibition on 'selling any in-game benefits for real-world money.' Minecraft and Mojang are not PayPal products; PayPal has no standing to enforce their guidelines on their behalf. PayPal suffered no damage from any of my account activities. The balance was nonetheless debited as PayPal's institutional 'damages.' PayPal changed its stated reason for this debit three times.

PayPal Executive Escalations Email

Date: June 2023

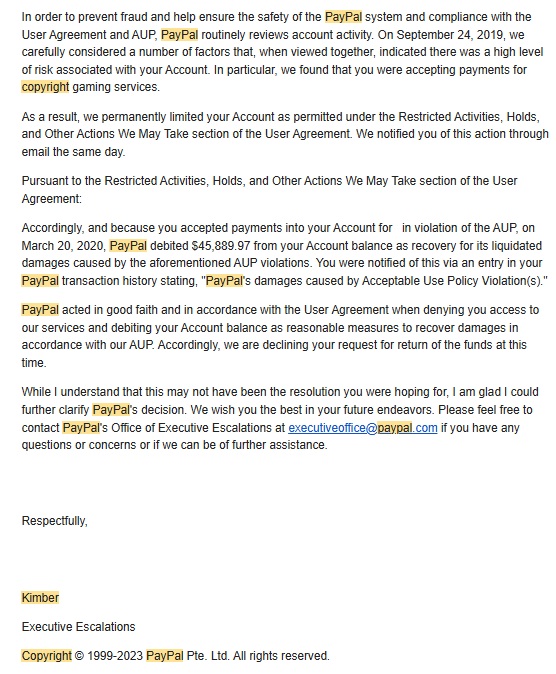

Key Statement: Allegation of "accepting payments for copyright gaming services" and reference to "liquidated damages". PayPal changed its stated reason for this debit three times. This correspondence also confirms PayPal's own account of the timeline: the account was limited on 24 September 2019 and the balance was debited on 11 March 2020. That is 169 days. PayPal had represented that funds would be returned after 180.

PayPal response referencing confidentiality

Date: June 2023

Key Statement: PayPal declared its decision and methodology permanently undisclosed as part of a 'proprietary review model.' The burden of proving actual damages rests with the party asserting them. PayPal made that assertion, appropriated USD 45,889.97 in the name of those damages, and then refused to produce any evidence to support them. Invoking confidentiality does not discharge that burden. It evades it.

PayPal Executive Escalations Email

Date: 10 September 2025

Key Statement: In direct response to the claimant's specific inquiry about the 11 March 2020 debit of USD 45,889.97, a PayPal Account Review employee named Cristofer stated in writing: 'The money belongs to you but is held in reserve to cover any disputes or reversals.' This was a signed response from a named human employee, addressed to a specific question about that specific debit.

PayPal's External Counsel Letter (April 2026)

Key Statement: Allegation of Nintendo copyright infringement as the basis for the AUP deduction.

Note: This is the third time PayPal has changed its stated reason for the deduction. The rationale was "Valve copyright infringement" in 2021, then "Minecraft Commercial Usage Guidelines" in 2023, and now "Nintendo copyright infringement" in 2026. In each instance, no proof of damages was provided, no complaint from the rights holder was produced, and no authorisation from either Nintendo or Mojang was shown. PayPal is not a legal representative of Nintendo or Mojang and has no standing to adjudicate their intellectual property rights on their behalf. These claims are refused.

External counsel's letter alleges 3,369 transactions in violation of the AUP. Applied literally to PayPal's own contractual rate of USD 2,500 per violation, that figure produces a total of USD 8,422,500, which is 183 times the USD 45,889.97 actually deducted. PayPal did not deduct USD 8,422,500. It deducted the available balance. That single arithmetic fact is a hallmark of an unenforceable penalty: the clause was not applied as a genuine pre-estimate of loss calibrated to the alleged violations. It was used to sweep whatever funds were present. Under the Dunlop/Denka framework applied by Singapore courts, a clause that produces a figure bearing no relationship to its own stated formula cannot constitute a genuine pre-estimate of loss and is an unenforceable penalty as a matter of law.

PayPal's External Counsel Letter Declining FIDReC Jurisdiction (April 2026)

Key Statement: PayPal, through external counsel, refuses to submit to FIDReC jurisdiction, citing Section 12.3 of the User Agreement and directing the claimant exclusively to Singapore courts.

Note: This refusal eliminates the only affordable dispute resolution avenue available to the claimant. It is also legally incorrect. PayPal's User Agreement expressly provides, at Section 12.2, that disputes may be resolved through "the Singapore International Arbitration Centre or any other established alternative dispute resolution ('ADR') provider mutually agreed upon by the parties." Section 12.3, which refers to Singapore courts, begins: "Except as otherwise agreed by the parties or as described in Section 12.2 above." External counsel's position inverts the plain text of the agreement: Section 12.3 is subordinate to Section 12.2, not the other way around. The refusal to submit to FIDReC is not grounded in the User Agreement. PayPal has declined three avenues of resolution: private settlement, disclosure of its claimed damages, and referral to FIDReC. The consistent refusal to engage through any affordable mechanism is inconsistent with good faith dispute resolution and the MAS fair dealing framework.

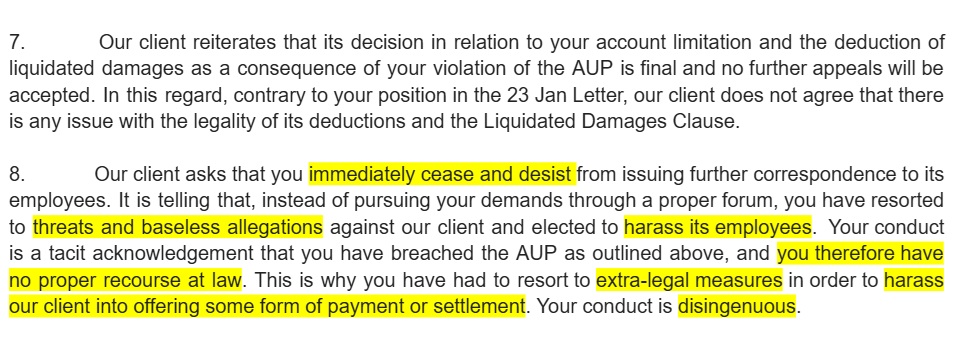

PayPal's External Counsel: Intimidation Response Following Regulatory Notification to Senior Management (April 2026)

In late March 2026, a formal notification with supporting documentation was sent directly to a senior executive of PayPal Pte. Ltd. The communication set out in detail why retaining customer funds without documented proof of actual harm is incompatible with the strict penalty doctrine under Singapore law, the PSA 2019 safeguarding framework, and MAS's Guidelines on Fair Dealing. It requested that PayPal either address those specific regulatory concerns or return the funds, and drew attention to the financial hardship caused by their continued withholding.

PayPal responded through external counsel approximately two weeks later, with no substantive engagement with any argument raised. Instead, the response instructed the claimant to cease issuing further correspondence to PayPal employees, described direct notification to Senior Management as "extra-legal measures" and "harassment," and stated that the claimant had "no proper recourse at law." The decision was declared final.

The response deployed quasi-legal intimidation language against an unrepresented retail consumer for the sole purpose of discouraging further regulatory escalation.

Note: Under MAS Guidelines on Fair Dealing [FSG-G04], Senior Management bear explicit, non-delegable responsibility for ensuring customers are treated fairly. Characterizing regulatory escalation to a licensed institution's Chief Executive as "harassment" is directly inconsistent with those obligations.

III. Business Context and Chronology

A. Commercial Activity

In 2019, the claimant engaged in digital commerce involving:

- Sale of virtual items for Team Fortress 2 and Minecraft;

- Provision of Discord server roles via DonateBot (donatebot.io) integration (website: donatebot.io; now defunct);

- Balance affected: USD 45,889.97 (per PayPal debit);

- Based on records available to the claimant in PayPal account activity, no chargebacks are shown.

B. Sequence of Events

IV. Analysis of Potential Legal Issues

Singapore law applies the penalty doctrine from Dunlop Pneumatic Tyre Co Ltd v New Garage and Motor Co Ltd [1915] AC 79, as clarified by the Court of Appeal in Denka Advantech Pte Ltd v Seraya Energy Pte Ltd [2020] SGCA 119. A liquidated damages clause may be unenforceable if it is out of all proportion to the legitimate interest in enforcement and operates as a deterrent rather than compensation.

Application: In June 2023, PayPal's Executive Escalations correspondence used differing rationales (Exhibits B and C) without identifying the specific transactions for either rationale. Without disclosure of whether the calculation incorporated assumptions based on (i) broad interpretations of third-party platform policies (for example Minecraft-related guidance) and/or (ii) unauditable third-party signals (for example legacy DonateBot.io logs), it is not possible to assess whether the USD 45,889.97 figure represents a genuine attempt at loss estimation or a mechanical sweep of the available balance based on unverified inputs.

Consequence of non-disclosure: PayPal has stated that its methodology is proprietary and will not be disclosed. Under the Dunlop/Denka framework, PayPal bears the burden of proving that the clause represents a genuine pre-estimate of loss. A refusal to produce the internal data, calculations, or records necessary to discharge that burden is not a neutral position: it means the burden cannot be discharged. A liquidated damages clause that cannot be shown to be a genuine pre-estimate of loss at the time of contracting is an unenforceable penalty as a matter of Singapore law, regardless of whether it appears in a signed agreement.

The Mathematical Anomaly: The arithmetic of the debit independently confirms this conclusion. PayPal's User Agreement stated liquidated damages of USD 2,500 per violation. USD 45,889.97 divided by USD 2,500 yields 18.35 violations. Since transactions are discrete units, 18.35 violations is a mathematical impossibility. This figure cannot represent a genuine application of the contractual formula. It is irreconcilable with the stated per-violation rate and cannot reflect a pre-estimate of loss. The most obvious alternative explanation is that the amount simply swept the available balance. Without an itemised breakdown, that explanation cannot be ruled out, and PayPal has refused to provide one.

On September 10, 2025, in direct response to the claimant's specific inquiry about the March 11, 2020 debit of USD 45,889.97, a PayPal representative named Cristofer stated in writing that "the money belongs to you but is held in reserve to cover any disputes or reversals" (Exhibit E). This was not an automated message: it was a signed written response from a named human employee, addressed specifically to the claimant's question about that debit, while PayPal continued to retain the balance. This written representation by PayPal activates promissory estoppel: PayPal made a clear and unequivocal representation of fact, the claimant relied on it by continuing to pursue resolution through correspondence rather than commencing proceedings, and it would be unconscionable to permit PayPal to resile from that representation.

PayPal cannot simultaneously acknowledge that the funds belong to the claimant and retain them as institutional "damages". The September 2025 statement is a written acknowledgment of the claimant's entitlement to the funds and is irreconcilable with the 2020 debit characterisation.

The second part of that statement introduces a further contradiction. PayPal stated the funds are held in reserve to cover "disputes or reversals", yet it has never identified any specific dispute or reversal that justified retaining the balance, let alone one capable of accounting for USD 45,889.97. If the funds were genuinely held to cover pending third-party claims, PayPal should be able to identify those claims, their amounts, and their current status. It has done none of this across six years of correspondence. The "disputes or reversals" rationale is therefore either an admission that no such claims exist, or a further instance of the shifting and unsubstantiated explanations that characterise PayPal's entire handling of this matter. Either way, it provides no legitimate basis for retention. It also directly undermines the 2020 "AUP damages" characterisation: if the funds were held as a reserve for third-party claims, they were not PayPal's damages to begin with.

Limitation Act consequences: The September 10, 2025 written acknowledgment constitutes an acknowledgment of the claimant's right to the funds within the meaning of the Limitation Act (Cap 163). This acknowledgment restarts the limitation period, extending the claimant's right to commence legal proceedings to approximately 2031. PayPal cannot rely on any limitation defence arising from the original 2020 debit.

PayPal is licensed by MAS as a Major Payment Institution and is subject to the Payment Services Act 2019 framework. The debited balance represented accumulated customer funds received from prior transactions. As such, it qualified as "relevant money" within the meaning of Section 23(14) of the PSA 2019, being money received from a customer that the Major Payment Institution continues to hold at the end of each business day.

Prohibition on set-off against customer funds: Regulation 16(1)(c) of the Payment Services Regulations 2019 mandates that a Major Payment Institution must "treat and deal with all the relevant money received from a customer as belonging to the customer." A financial institution cannot unilaterally appropriate customer funds to satisfy an alleged institutional debt or claim without a customer instruction or a court order. The 2020 debit, characterised as PayPal's own "damages", is a direct appropriation of customer funds for PayPal's own benefit in violation of this principle. PayPal's own 2025 written confirmation that "the money belongs to you but is held in reserve to cover any disputes or reversals" further acknowledges the customer-property character of the funds, making the 2020 debit irreconcilable with Regulation 16(1)(c). Notably, if the funds were held in reserve for disputes or reversals, they were safeguarded customer money and not PayPal's institutional property to appropriate as "damages".

Additional PSA safeguarding provisions engaged: Section 23(2) requires deposit of relevant money in a trust account no later than the next business day. Section 23(7) restricts the use of trust account moneys for the payment of the debts of the Major Payment Institution. Converting customer funds into institutional "damages" without a court order or customer instruction is inconsistent with both provisions.

The "Notice for non-Singapore residents" cannot apply retroactively: PayPal's disclosure "Terms under the Singapore Payment Services Act 2019" containing the non-resident safeguarding exception was added on 27 June 2023, more than three years after the 11 March 2020 debit. At the time of the debit, no such exception had been published or communicated to the claimant. PayPal cannot rely on a policy disclosure published in 2023 to retrospectively characterise as unsafeguarded funds that were held and debited in 2020. At the material time, the funds were subject to the safeguarding framework applicable to a Singapore-licensed MPI without the benefit of the 2023 carve-out.

PayPal's conduct constitutes an unfair practice under the Consumer Protection (Fair Trading) Act (CPFTA) on multiple grounds.

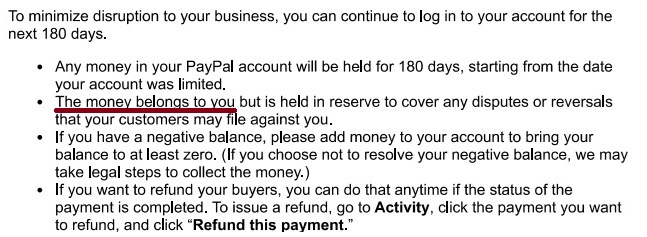

Misleading representation as to fund availability: PayPal communicated to the claimant that her funds would become available after a defined holding period of 180 days. That representation was false. The funds were not released at 180 days. They were not released at all. They were permanently confiscated 11 days before the represented period had even elapsed, without notice, without particulars, and without any contemporaneous explanation. Under section 4(a) of the CPFTA, a supplier engages in an unfair practice if it makes a false claim. The 180-day availability representation was either knowingly false at the time it was made, or became actionable when PayPal chose to act in direct contradiction to it.

Material omission: Under section 4(b) of the CPFTA, a supplier also engages in an unfair practice if it employs deceptive or misleading tactics, including through omission of material information. At no point before the March 2020 debit did PayPal inform the claimant that: (i) her balance was at risk of being taken as institutional damages; (ii) a debit rather than a release was contemplated; or (iii) PayPal considered itself entitled to appropriate the entire balance unilaterally. The claimant was kept in structured ignorance while the debit was prepared and executed. That omission is not incidental. It is what made the debit possible.

Shifting and contradictory explanations as an unfair practice: The CPFTA reaches conduct that, taken as a whole, is unfair having regard to the circumstances. PayPal provided three materially different explanations for the same debit across multiple years: "AUP damages" (2020), "accepting payments for copyright gaming services" (June 2023, Exhibit C), and "Minecraft Commercial Usage Guidelines" (June 2023, Exhibit B). It then declared the underlying methodology permanently confidential as a "proprietary review model." A consumer who receives three different explanations across six years, followed by a refusal to disclose any supporting records, has been subjected to a sustained pattern of misleading conduct. Taken together, that pattern constitutes an unfair practice under the Act regardless of which individual representation is assessed in isolation.

PayPal's conduct in connection with the 180-day holding period constitutes three distinct and sequential breaches of contract, all arising from the same promise made to the claimant at the moment of account limitation.

First breach (failure to notify): PayPal represented that it would contact the claimant after the 180-day holding period to advise her how to access her funds. It never did. No proactive communication was sent to the claimant in the period leading up to or following the debit. She was not informed that the retention period was ending, that a debit was being contemplated, or that her funds were at risk of permanent confiscation. She discovered what had happened only when she logged into her own account and observed the balance had been taken. PayPal's silence during that period was not an oversight. It was a breach of a specific, communicated promise to keep the claimant informed, and that silence made every subsequent breach possible.

Second breach (early debit: 169 days, not 180): The account was permanently limited on September 24, 2019. The balance was debited on March 11, 2020. That is 169 days. Not 180. PayPal's own communications represented that funds would be available after 180 days. PayPal executed the debit 11 days before that period had elapsed. This is not a procedural technicality. It is a breach of a specific promise made to the claimant at a moment of acute financial vulnerability, on the same day the WHO declared COVID-19 a global pandemic, when the funds constituted essential subsistence resources.

Third breach (wrongful appropriation instead of release): The 180-day representation carried an unmistakable implication: at the end of the holding period, the funds would be returned to the claimant. Instead, PayPal permanently appropriated them as alleged "AUP damages." The claimant was told her money would be held and then made available. It was instead taken, without notice, without particulars, without itemisation, and without any prior indication that confiscation rather than release was what PayPal intended. The contractual basis for that taking has never been coherently explained in over six years of correspondence.

These three breaches are not independent failures. They form a sequence: PayPal made a promise it did not intend to keep, stayed silent while the deadline approached, acted before it arrived, and took the money rather than returning it. At every step where it was obliged to act transparently, PayPal did the opposite.

PayPal appropriated USD 45,889.97 from the claimant's balance. It has never produced proof of damages, a valid contractual basis, or a coherent calculation. On any of those grounds independently, the deduction fails: it is an unenforceable penalty, or it was not calculated in accordance with the stated formula, or it was made without lawful authority. Where a payment is made and the basis for that payment wholly fails, the law requires it to be returned. This is not a contingent or marginal argument. It is a straightforward claim for money had and received. PayPal holds USD 45,889.97 that belongs to the claimant, for which it has provided no valid legal justification in over five years of correspondence. It must be returned.

The term relied upon to justify the debit is subject to a Unfair Contract Terms Act (UCTA) reasonableness analysis. The clause, as applied, operates as a self-help right to appropriate customer funds, and/or as an indemnity or limitation of PayPal's liability, written into standard-form terms presented to consumers on a take-it-or-leave-it basis. Under UCTA, PayPal bears the burden of establishing that the term satisfies the reasonableness requirement. A clause that purports to authorise appropriation of USD 45,889.97 from a consumer's balance, without notice, without itemisation, and without any documented actual loss, cannot plausibly satisfy that standard.

As a Major Payment Institution licensed by MAS, PayPal is subject to the MAS Guidelines on Fair Dealing (FSG-G04, effective 30 May 2024), which require boards and senior management to ensure that fair dealing outcomes are delivered to all customers across all products and services.

Outcome 1: Institutional culture of fair dealing: Six years of non-response, shifting explanations, and refusal to provide particulars for a debit of USD 45,889.97 is irreconcilable with a genuine institutional culture of fair dealing. The debit was executed without disclosing what damages PayPal actually suffered. Subsequent correspondence provided three different and contradictory explanations across multiple years. This pattern is inconsistent with the expectation that boards and senior management champion fair dealing as a foundational institutional value.

Outcome 4: Clear, relevant and timely information: PayPal has never provided clear, relevant, or timely information about the basis for the debit. The claimant was directed to broad policy language instead of record-based particulars. Explanations shifted from "AUP damages" to "copyright gaming services" to Minecraft's Commercial Usage Guidelines, all without transaction-level evidence. PayPal then declared its methodology permanently undisclosed as part of a "proprietary review model". This is a sustained, six-year failure of the information standard required under Outcome 4.

Outcome 5: Independent, effective and prompt complaints handling: PayPal's complaints process in this matter operated as a mechanism of attrition rather than resolution. After six years of formal complaints, the claimant has never been told what damages were suffered, how they were quantified, or what records support the decision. No complaint process that produces this outcome over six years can be described as independent, effective, or prompt. The MAS guidelines are explicit that systemic complaint failures must be addressed through trend analysis and structural remediation.

The debit of USD 45,889.97 was executed on 11 March 2020, the same day the World Health Organisation declared COVID-19 a global pandemic. The claimant is a resident of Argentina for whom these funds represented essential subsistence resources. The debit was executed without notice, without particulars, in breach of PayPal's own 180-day representation, and at the precise moment of maximum external financial shock to individuals and households globally.

MAS issued guidance during the COVID-19 period calling on financial institutions to exercise heightened sensitivity and support toward customers experiencing financial difficulty. PayPal's conduct, executing a large, opaque, unilateral debit against a customer with no documented loss, no calculation, and no itemisation, at the height of a global economic crisis, is inconsistent with those expectations and with the fair dealing principle that institutions must consider the needs and interests of vulnerable customers.

The MAS Fair Dealing Guidelines (FSG-G04) explicitly require financial institutions to give extra consideration to customers who are more vulnerable, including those facing financial hardship or difficult personal circumstances. A financial institution that responds to six years of demands for basic accountability with boilerplate deflection has not given any consideration to the claimant's circumstances, let alone the extra consideration the guidelines require.

As a licensed Major Payment Institution, PayPal is subject to MAS's technology risk management guidelines and the general governance expectations applicable to Singapore-licensed payment service providers. These include the obligation to maintain adequate records supporting material decisions affecting customer funds, and to implement governance frameworks ensuring that enforcement actions of this type are subject to human review, documented approval, and audit trail retention.

PayPal has been unable, after six years of written demands and a formal Letter of Demand, to produce: (i) the internal decision record supporting the 11 March 2020 debit; (ii) the basis used to determine the quantum of USD 45,889.97; (iii) the identity and role of the reviewer(s) who authorised the debit; (iv) any contemporaneous documentation linking the debit to a quantified, actual loss suffered by PayPal; or (v) any third-party data inputs that were relied upon and whose integrity can be tested.

The inability to produce any of these records after six years is a governance and recordkeeping compliance failure. A licensed MPI executing a debit of this size must be able to reconstruct that decision from its own internal records. If it cannot, that is not a customer service issue. It is a material compliance deficiency under the PSA 2019 framework.

MAS technology risk management guidance further highlights governance and oversight expectations for material automated decisions and third-party data dependencies. If the debit was executed automatically based on third-party platform signals (such as DonateBot.io integration data or Minecraft policy flags), PayPal should be required to demonstrate that such automated decisions were subject to adequate human oversight, that the third-party data inputs were independently verified, and that audit records were retained. DonateBot.io is no longer publicly accessible or auditable, which means any reliance on its data cannot be independently tested without PayPal disclosing its own records.

PayPal has implied in its communications that the underlying activity was unlawful, specifically citing "copyright issues". That position is irreconcilable with retaining the same funds as institutional "AUP damages." Under section 39 of the Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act (CDSA) (now section 45), a financial institution that genuinely believes funds are linked to unlawful conduct is required to file a Suspicious Transaction Report (STR) with STRO, not appropriate those funds for its own benefit.

The consequence is unavoidable: if PayPal believed the funds were connected to unlawful activity, it should have filed an STR and left disposition to the authorities. If it did not file an STR, that is affirmative evidence it did not genuinely hold that belief, and the insinuations of illegality are unfounded. Either way, PayPal has no legitimate basis to retain the funds. The absence of an STR strips away the only remaining implied rationale for the deduction.

V. Outstanding Accountability Gaps

Despite repeated written demands over six years, including a formal Letter of Demand issued in January 2026, PayPal has systematically refused to provide basic accountability for the USD 45,889.97 debit. The following information has been demanded multiple times and has never been disclosed:

Threshold Issue: Proof of Damages

PayPal has never produced documentary evidence of what actual loss or harm it suffered as a result of the claimant's alleged activity. No contemporaneous record. No quantified harm. No identified transaction causing specific loss. The funds were taken in the name of "damages"; no evidence of those damages has ever been shown.

Calculation and Methodology

- Transaction IDs of each alleged violating transaction;

- Specific AUP provisions allegedly breached per transaction;

- Itemised breakdown: how USD 45,889.97 was calculated (18.35 violations at USD 2,500 each is mathematically impossible for discrete transactions);

- Evidence that the contractual liquidated damages formula was actually applied rather than simply sweeping the available balance;

- Methodology: whether the calculation incorporated broad interpretations of third-party platform policies (Minecraft guidelines) or unauditable third-party signals (DonateBot.io logs);

- Evidence of customer complaints, chargebacks, or reversals at the time of the debit.

Shifting and Contradictory Rationales

PayPal gave different and inconsistent explanations for the same debit. In its 2020 transaction record, the debit was labelled simply as "AUP damages." In June 2023, PayPal's Executive Escalations team stated the review "found that you were accepting payments for copyright gaming services" (Exhibit C). In a separate June 2023 communication, the basis shifted again to Minecraft's "Commercial Usage Guidelines" and "selling any in-game benefits for real-world money" (Exhibit B). PayPal then declared the underlying methodology permanently confidential as part of its "proprietary review model" (Exhibit D). Three materially different explanations across multiple years, followed by a refusal to disclose any supporting records, is not a legitimate exercise of commercial confidentiality. It is a pattern of deflection that makes independent verification of the debit's basis impossible.

The claimant disputes that either framing accurately describes her activity. The published Minecraft commercial usage guidance does not categorically prohibit selling in-game items or server perks for real-world money. If PayPal relies on either the copyright gaming services theory or the Minecraft guidelines theory, that reliance must be tied to specific contractual language and discrete, identified transactions rather than broad categorical labels applied without particulars.

If PayPal relied on third-party platform signals, any reliance on DonateBot.io raises additional and unresolved questions. DonateBot.io has been defunct for several years and is no longer publicly accessible or auditable. It was reported within the Discord community for occasional role or perk mis-assignments across servers, which could generate inaccurate records. PayPal cannot rely on data from a source that no longer exists, has never been disclosed, and cannot be independently tested. Without disclosure of what DonateBot.io data was used and how it was verified, the integrity of any such input cannot be assessed.

Safeguarding and Regulatory Compliance (PSA 2019)

- Whether the debited balance qualified as "relevant money" under Section 23(14) of the PSA 2019 at the time of the debit, and when (if ever) it ceased to qualify;

- The safeguarding method used for the relevant period: trust account, guarantee, or undertaking;

- The account structure and legal entity under which the funds were received and safeguarded;

- Ledger mechanics: which accounts were reduced, which were credited, and whether funds were transferred into a PayPal-owned account;

- The contractual and statutory authority relied upon to appropriate safeguarded customer funds for PayPal's own benefit without customer instruction or judicial order, and how that authority is reconciled with Regulation 16(1)(c) of the Payment Services Regulations 2019 (which mandates treating customer money as belonging to the customer);

- The precise nature of the "loss" being recovered, including whether any third-party claims, disputes, or reversals existed at the time of the debit.

Decision Process and Governance

- Internal decision record supporting the 11 March 2020 debit;

- Identity and role of the reviewer(s) who authorised the debit;

- Whether the decision involved human review or was executed automatically;

- Third-party data sources relied upon: whether the decision incorporated reports, flags, or integration data from DonateBot.io or any similar third-party source, including any third-party allegations characterised as "copyright" issues;

- If third-party data was used: audit records demonstrating that such inputs were independently verified and that automated decisions were subject to adequate human oversight;

- Whether the decision basis relied on a Minecraft policy interpretation, and if so, the specific contractual language and discrete transactions supporting that interpretation.

180-Day Hold Representation

- All messages shown to the claimant regarding the 180-day holding period, including timestamps;

- Reconciliation of those messages with the March 11, 2020 debit date (169 days after the September 24, 2019 account limitation);

- Explanation for debiting the balance 11 days before the represented 180-day period expired.

UCTA and PDPA Concerns

- Whether the relied-upon term functions as (i) an indemnity, (ii) an exclusion or limitation of PayPal's liability or duties, or (iii) a self-help right to appropriate customer funds;

- The exact clause text and User Agreement version relied upon;

- Internal flags, risk markers, or scores applied to the account following the AUP classification;

- Whether any such data was shared with third parties (payment networks, fraud prevention networks, or other financial institutions);

- The categories of recipients and dates of any such transmission.

The refusal to provide this information is not a secondary matter of procedure or commercial confidentiality. It is a foundational accountability failure. PayPal has appropriated USD 45,889.97, labeled it as institutional "damages," and then systematically refused to demonstrate that any damages were suffered, how they were quantified, or under what legal authority the debit was executed. A licensed Major Payment Institution executing a debit of this magnitude must be able to reconstruct that decision from its own internal records. After six years and a formal Letter of Demand, PayPal has produced none of this. That failure is itself a material regulatory concern under the PSA 2019 framework.